You can download a PDF of this article to print or email here

Introduction

Aegis is one of the highest risk brokerage firms in the country and is using its retail customer accounts to stuff the worst underwritings in the country. Sadly, unless some authority stops Aegis, an update later in the year will show further investor wreckage as a result of Aegis's disregard for its most basic duties.

In March 2024, we documented that Aegis was systematically underwriting spectacularly failing nano-cap stocks in a previous post. We concluded that investors, including many Aegis' retail customers, suffered $3.0 billion to $5 billion in losses in recent years as a result of Aegis' conduct.

You can read that post, "Aegis Capital is Farm-to-Table Securities Fraud Purveyor, Harming Investors at Least $5 Billion!" LinkedIn here or on our website here.

In the three months since we published our research into Aegis underwritings, Aegis has continued - unabated - to harm investors through its underwriting activities. In this post, we briefly summarize our prior findings and demonstrate the ongoing investor harm being perpetrated by Aegis.

Prior Findings

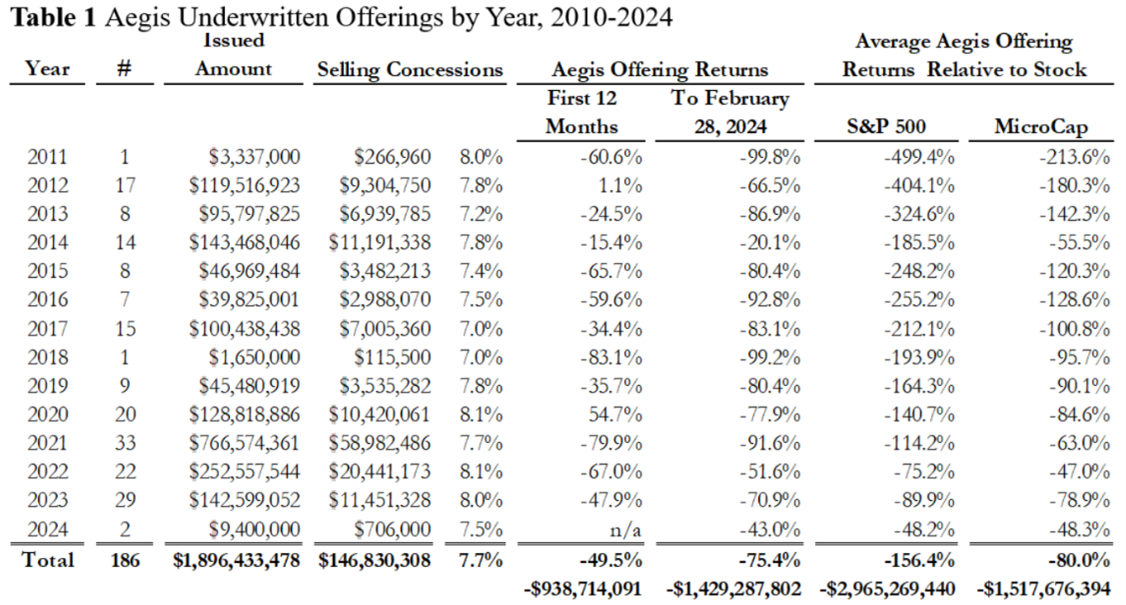

Table 1 from our prior post partially captured investors' experience with Aegis underwritings, although it misses the bid-ask spreads and markup and markdowns which were substantial.

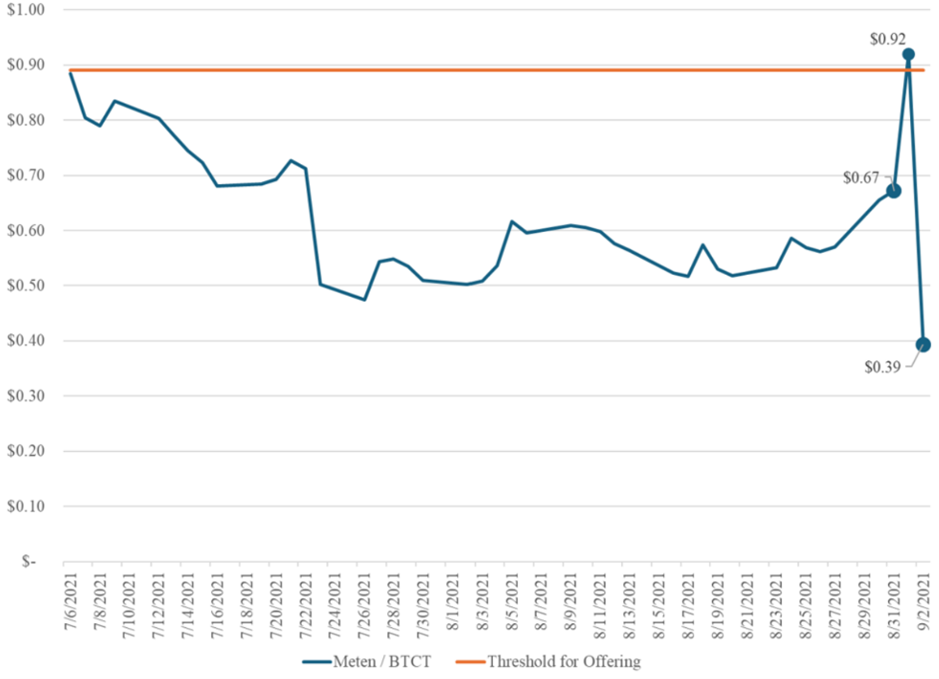

We also concluded that in at least three instances Aegis marked the close or looked the other way while others marked the close to facilitate an underwriting. We described one of these examples, Meten. Figure 1, excerpted from our earlier post, shows the dramatic, unexplained (we think the explanation is obvious) one-day spike in Meten's stock price which facilitated Aegis's underwriting.

In a follow-up, we described facts leading us to conclude that someone marked the close in SeaChange International to facilitate that Aegis underwriting. We also illustrated how an issuer and underwriter might game the dilution disclosure when the issuer is burning through resources at a rapid pace, as was true of virtually all the Aegis underwritten issuers we reviewed. You can read that post, "Another Example of Apparent Marking-the-Close" on LinkedIn here or on our website here.

SeaChange's closing stock price declined 72.3% from $3.72 on March 31, 2020 to $1.03 on March 26, 2021, before spiking to close at $2.08 on March 29, 2021 and then continuing its decline to $0.08 on a split-adjusted basis on February 28, 2024. See Figure 2, excerpted from our SeaChange post.

Figure 2 SeaChange Daily Closing Price, March 31, 2020 to March 18, 2024

The fleeting spike in SeaChange's closing price to $2.08 the day before the offering occurred with no material news but on extraordinary volume. Trading in SeaChange on March 29, 2021 drove the price up throughout the day to close at $2.08. The issuer and the underwriter benefited from this activity as it allowed the issue size to be larger. If SeaChange had closed above $2.40, the issue size would not have been limited at all but the effort to push the closing price higher appears to have run out of juice.

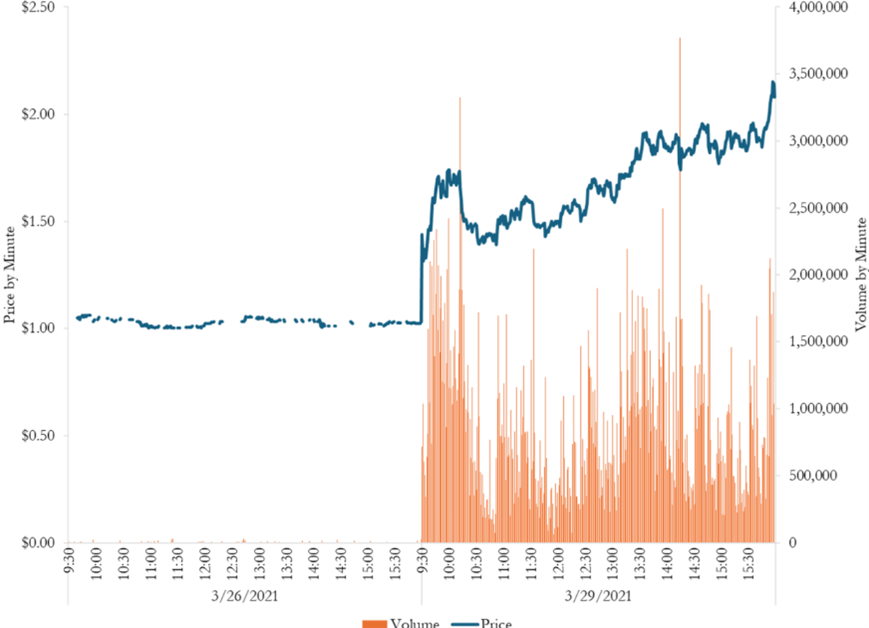

The trading volume on March 29, 2021 was 440 times the trading volume on March 26, 2021 and 12 times the float. In fact, the average trading volume per minute on March 29, 2021 was roughly equal to the trading volume for the entire day on March 26, 2021. See Figure 3, excerpted from our SeaChange post.

Figure 3 SeaChange Intraday Price and Volume, March 26 and March 29, 2021

Aegis Keeps on Harming Investors in 2024

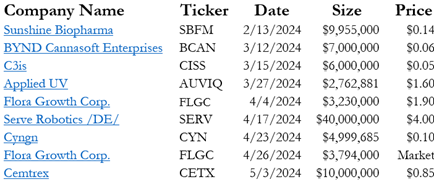

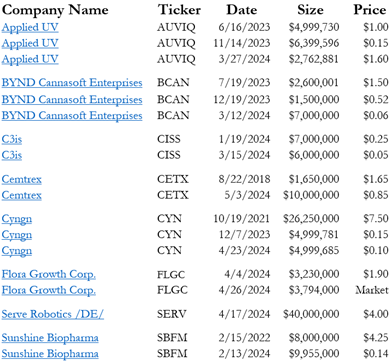

At the time we first posted about Aegis's underwritings, Aegis had underwritten two offerings in 2024. Between mid-February and the end of May 2024, Aegis underwrote 9 offerings totaling $95 million for 8 issuers listed in Table 2.

Table 2 Aegis's Underwritings February 1, 2024 - May 31, 2024

As is typical of the other issuers Aegis underwrites, these 8 issuers were small failing firms in which no uninformed retail investors should invest. Of course, the issuers' laughable condition - if what Aegis is doing to investors was only funny - was well known to Aegis as the underwriter in these offerings. But it's even worse; 6 of the 8 issuers were companies whose securities Aegis had previously underwritten with disastrous results for Aegis's investors. See Table 3.

Table 3 Aegis's Recent Underwritings with Companions

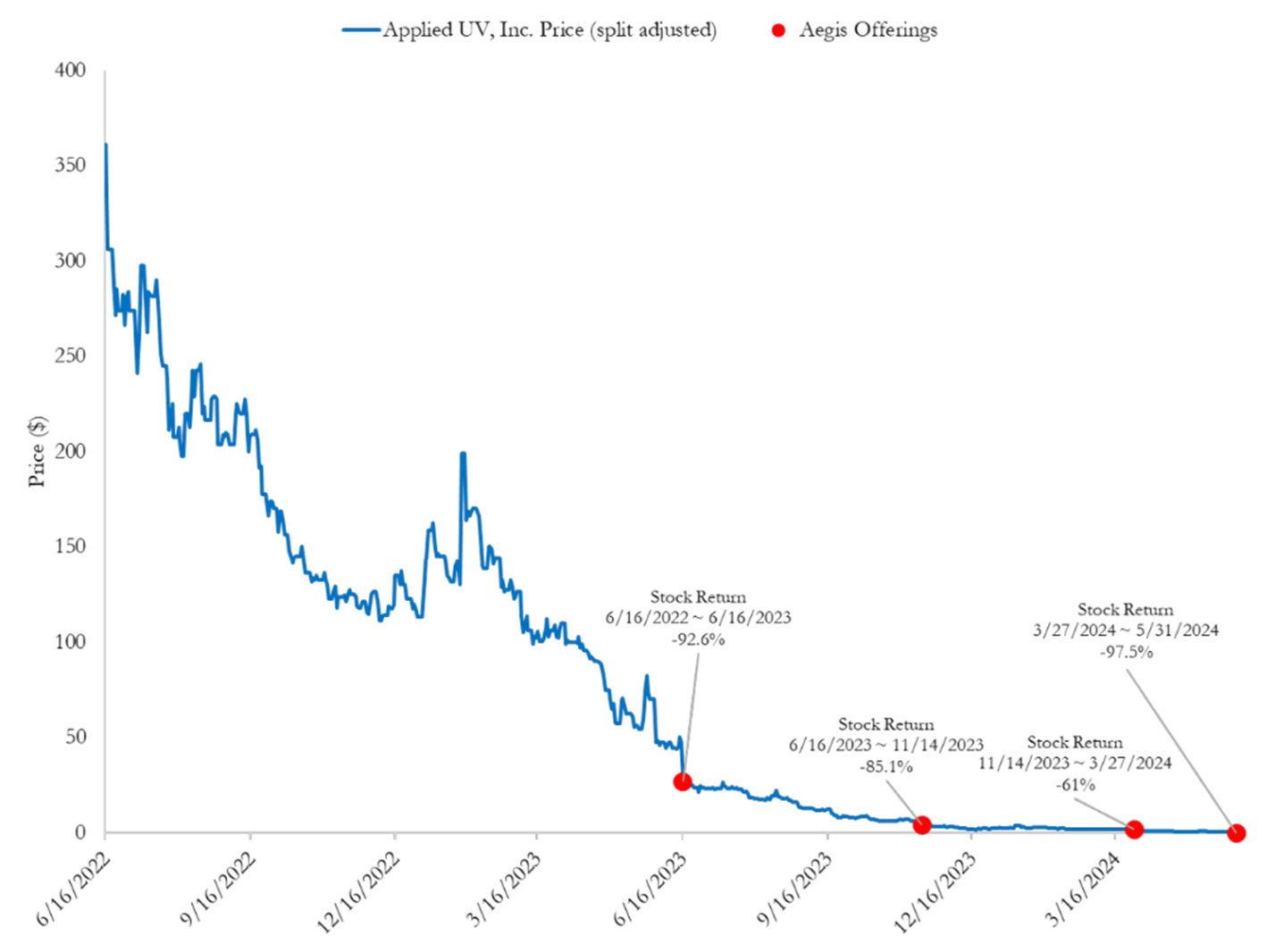

Applied UV

Aegis underwrote a $2,762,881 offering for Applied UV on March 27, 2024 after underwriting 2 previous Applied UV offerings totaling $11.4 million in the past 12 months. The three 424bs can be located here, here and here.

Applied UV's stock price had declined 92.6% over the one year prior to the first Aegis underwriting.

Applied UV's stock price dropped another 85.1% over the five months between Aegis' first and second underwritings and a further 61% between Aegis's second and third underwritings.

In the two months between the last Applied UV underwriting and May 31, 2024, the stock price dropped 97.5%.

Cumulatively in the past two years Applied UV's stock price has dropped 99.99% while Aegis was underwriting its securities offerings.

Figure 4 Aegis's Applied UV Securities Offerings

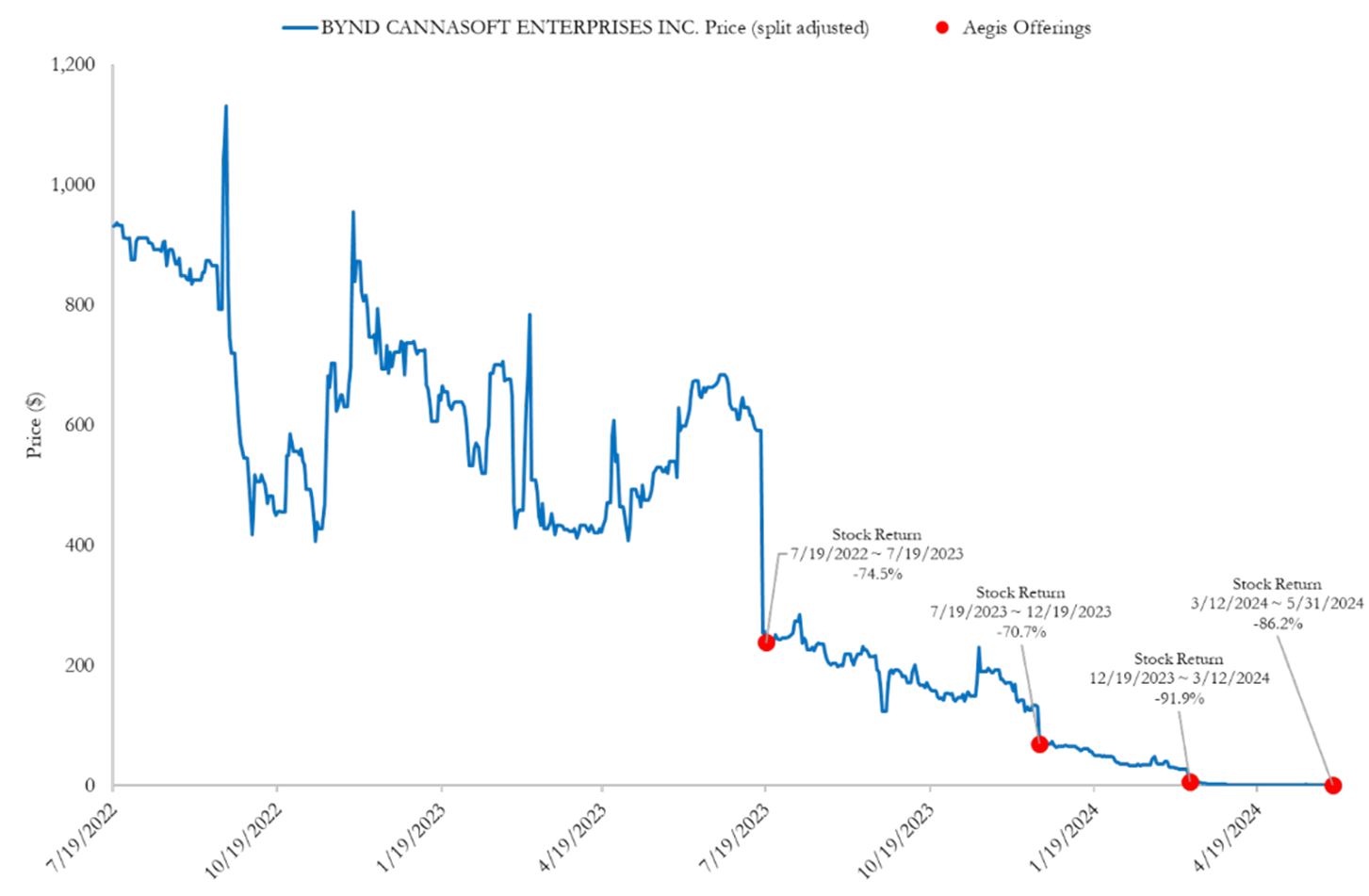

BYND Cannasoft Enterprises

Aegis underwrote a $7,000,000 offering for BYND Cannasoft on March 12, 2024 after underwriting 2 previous BYND Cannasoft offerings totaling $4.1 million in the previous 9 months. The three 424bs can be located here, here and here.

BYND Cannasoft's stock price had declined 74.5% over the one year prior to the first Aegis underwriting.

BYND Cannasoft's stock price dropped another 70.7% over the five months between Aegis' first and second underwritings.

BYND Cannasoft's stock price dropped a further 91.9% between Aegis's second and third underwritings.

In the two and a half months between the last BYND Cannasoft underwriting and May 31, 2024, the stock price dropped another 86.2%.

Cumulatively in the past two years BYND Cannasoft's stock price has dropped 99.92% - from $931 to $0.77 - while Aegis was underwriting its securities offerings.

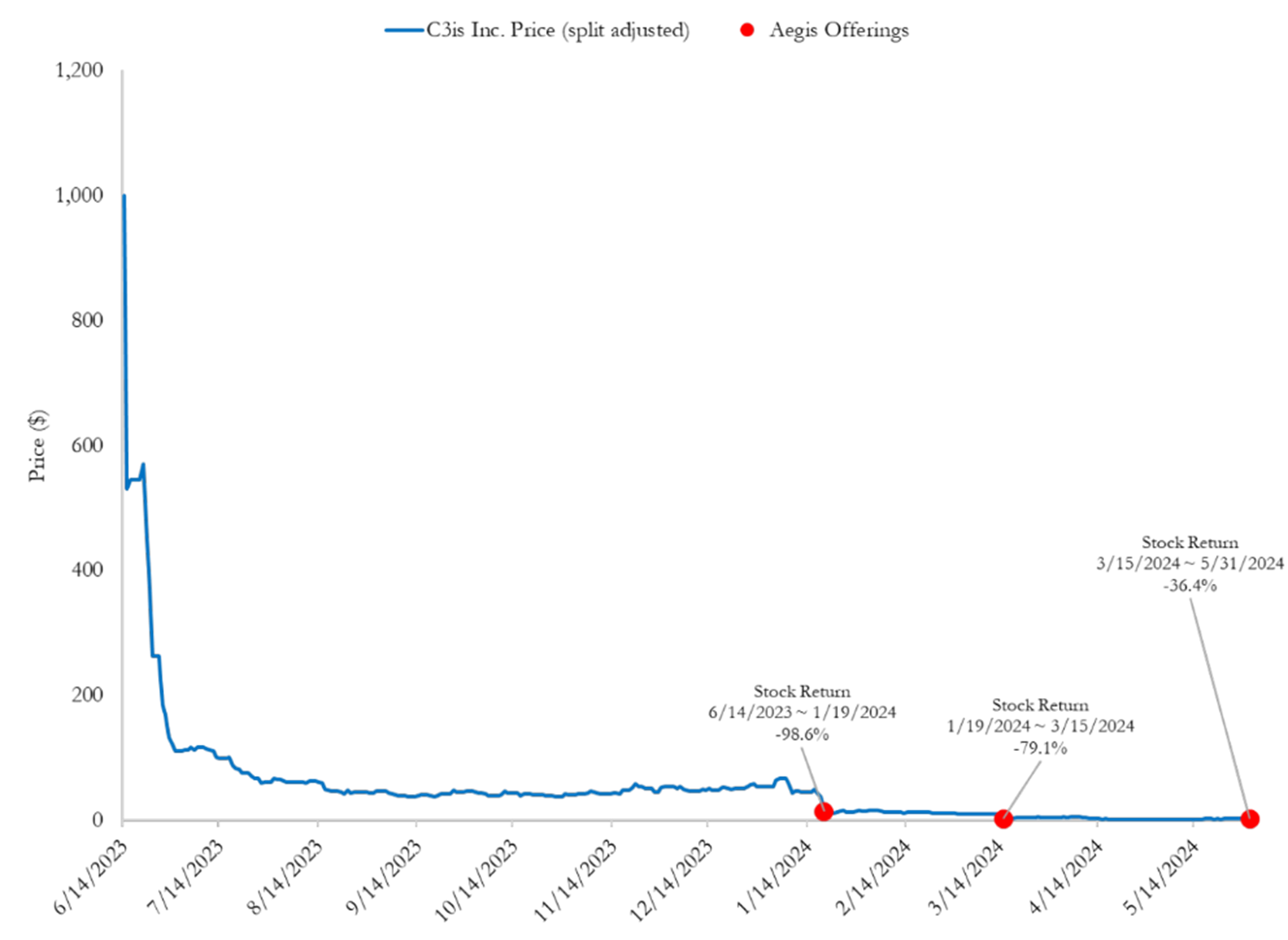

Aegis underwrote a $6,000,000 offering for C3is on March 15, 2024 after underwriting a previous $7,000,000 C3is offering 2 months earlier. The two 424bs can be located here and here.

C3is's stock price had declined 98.6% over the 7 months prior to the first Aegis underwriting in January 2024.

C3is's stock price dropped another 79.1% over the two months between Aegis' first and second underwritings.

In the two and a half months between the last C3is underwriting and May 31, 2024, the stock price dropped 36.4%.

Cumulatively, in just one year, C3is's stock price has dropped 99.92% - from $1,000 to $1.80 - while Aegis was underwriting its securities offerings.

Figure 6 Aegis's C3is Securities Offerings

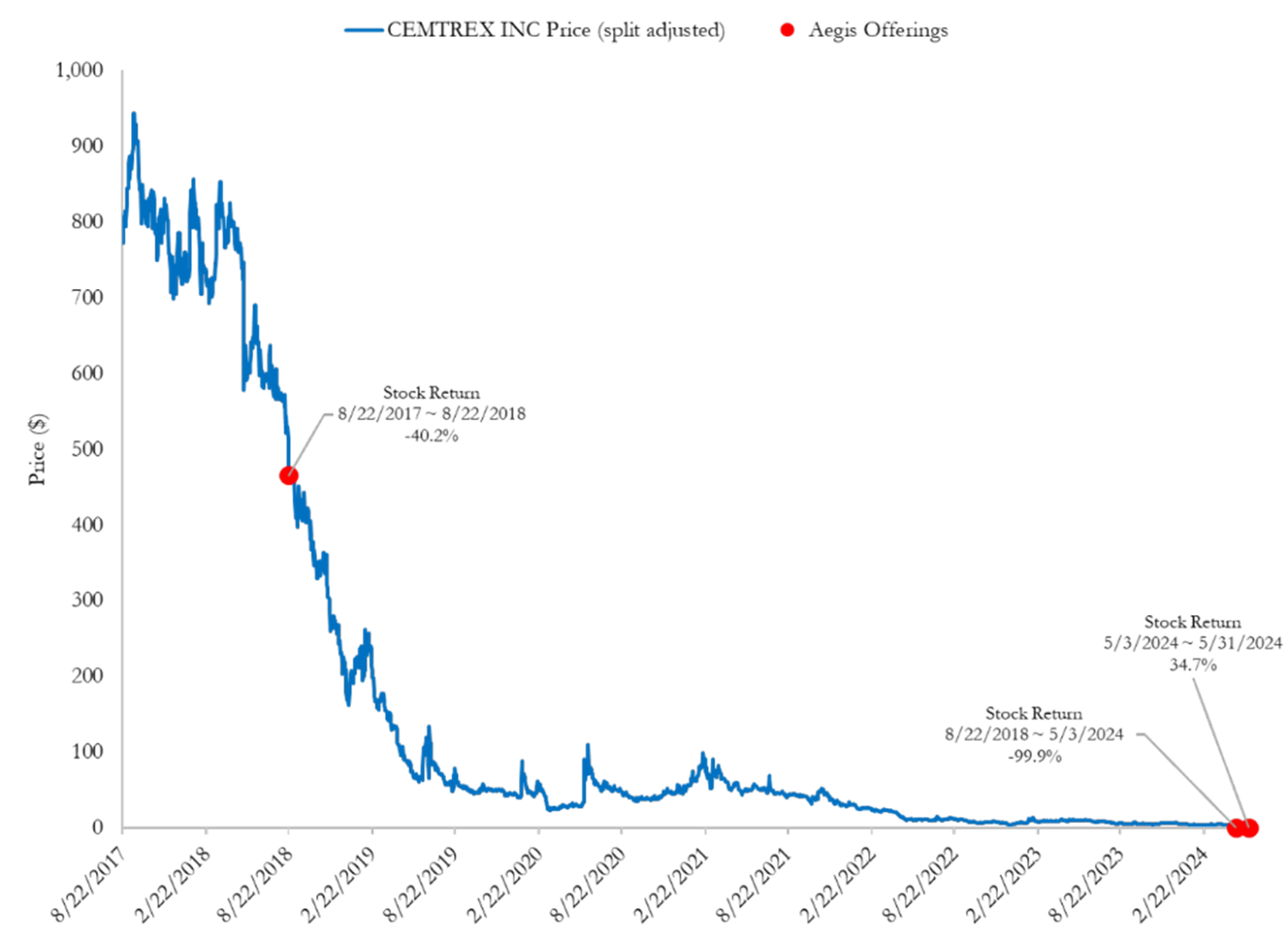

Cemtrex

Aegis underwrote a $10,000,000 offering for Cemtrex on March 15, 2024 after underwriting a $1,650,000 Cemtrex offering in 2018. The two 424bs can be located here and here.

Cemtrex's stock price had declined 40.2% over the 12 months prior to the first Aegis underwriting in August 2018.

Cemtrex's stock price dropped another 99.9% over the nearly six years between Aegis' first and second Cemtrex underwritings.

In four weeks between the last Cemtrex underwriting and May 31, 2024, the stock price increased 34.7 but has since dropped below the May 3, 2024 issue date price.

Cumulatively, Cemtrex's stock price has dropped 99.7% while Aegis was underwriting its securities offerings.

Figure 7 Aegis's Cemtrex Securities Offerings

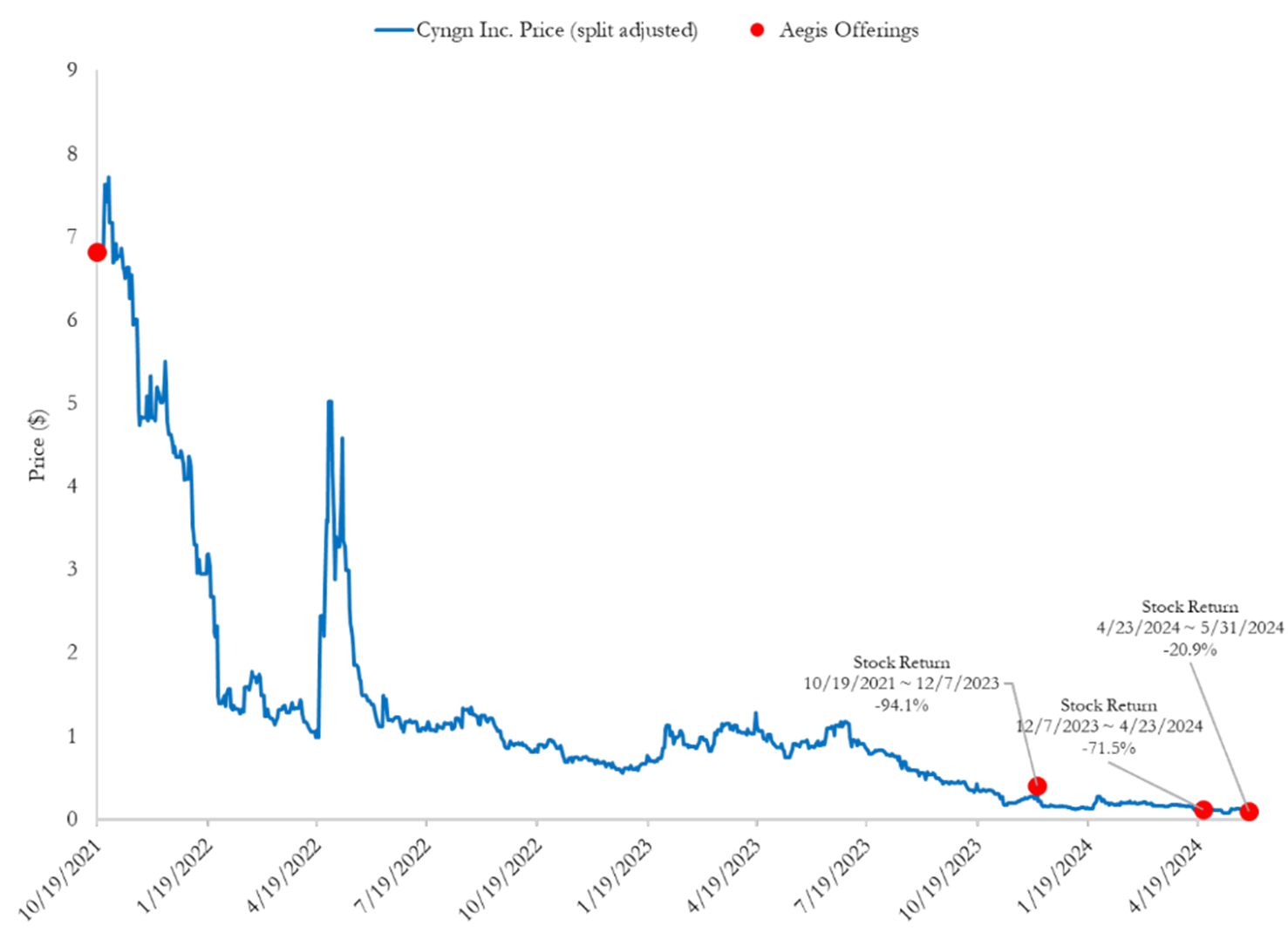

Cyngn

Aegis underwrote a $4,999,999 offering for Cyngn on March 12, 2024 after underwriting 2 previous Cyngn offerings totaling $31,250,000 in the previous 2 years. The three 424bs can be located here, here and here.

Aegis underwrote Cyngn's initial public offering on October 19, 2021.

The stock declined 94.1% over the next two years immediately preceding Aegis's second Cyngn underwriting.

Cyngn's stock price dropped another 71.5% over the five months between Aegis' second and third underwritings.

In the five weeks months between the last Cyngn underwriting and May 31, 2024, the stock price dropped another 20.9%.

Cumulatively, in the past two years and eight months, Cyngn 's stock price has dropped 98.7% while Aegis was underwriting its securities offerings.

Figure 8 Aegis's Cyngn Securities Offerings

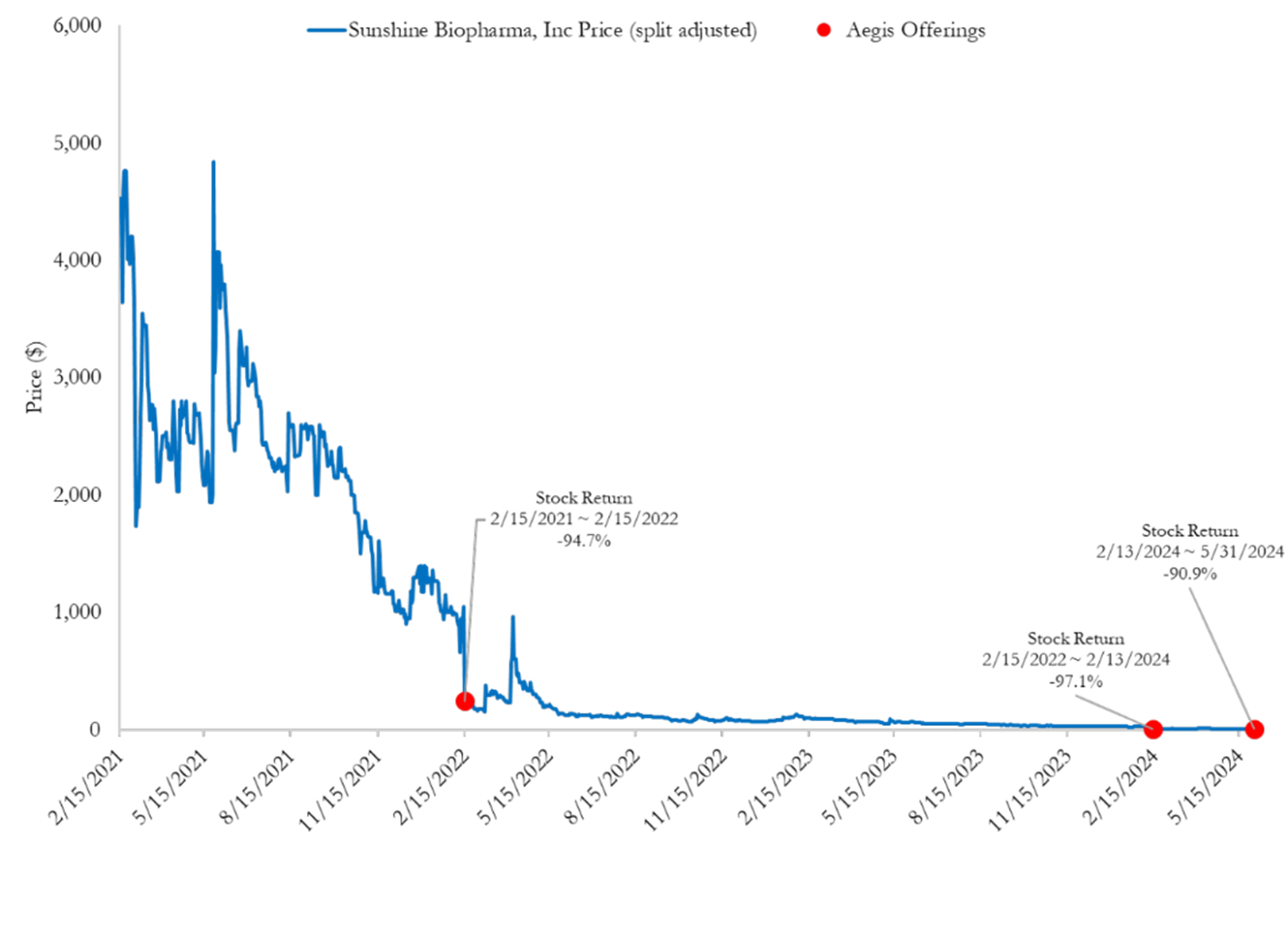

Sunshine Biopharma

Aegis underwrote a $9,955,000 offering for Sunshine Biopharma on February 13, 2024 after underwriting a previous $8,000,000 Sunshine Biopharma offering 2 years ago. The two 424bs can be located here and here.

Sunshine Biopharma's stock price had declined 94.7% over the one year prior to the first Aegis underwriting.

Sunshine Biopharma's stock price dropped another 97.1% over the two years between Aegis' first and second underwritings.

Sunshine Biopharma's stock price dropped a further 90.9% in the three and a half months between the last Sunshine Biopharma underwriting and May 31, 2024.

Cumulatively in the past two years Sunshine Biopharma's stock price has dropped 99.99% while Aegis was underwriting its securities offerings.

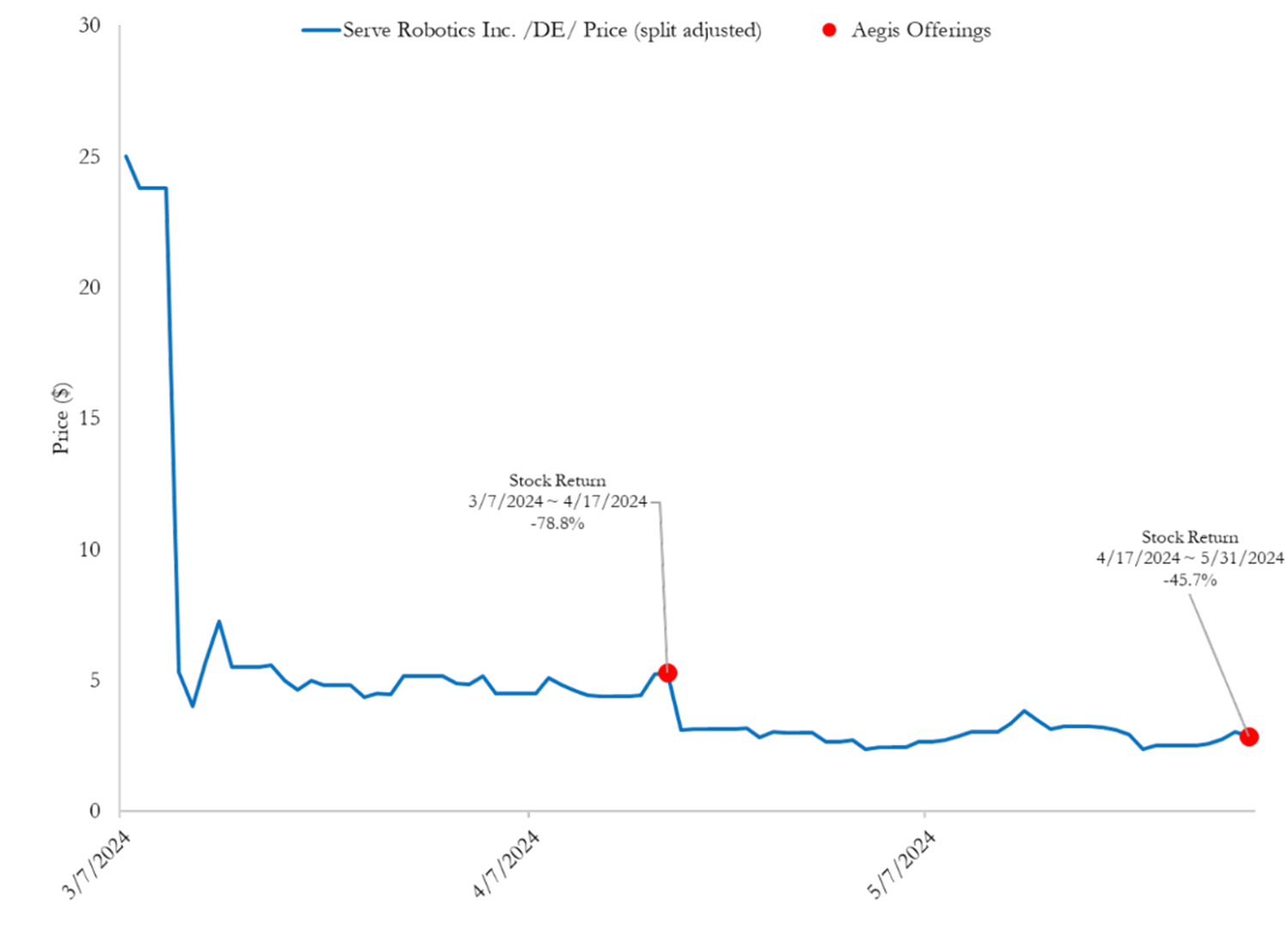

The six Aegis underwritten issuers discussed above were all issuers Aegis had underwritten prior to February 2024 and have underwritten follow-on offerings since. For completeness, we next discuss two issuers Aegis underwrote for the first time in the past few months.

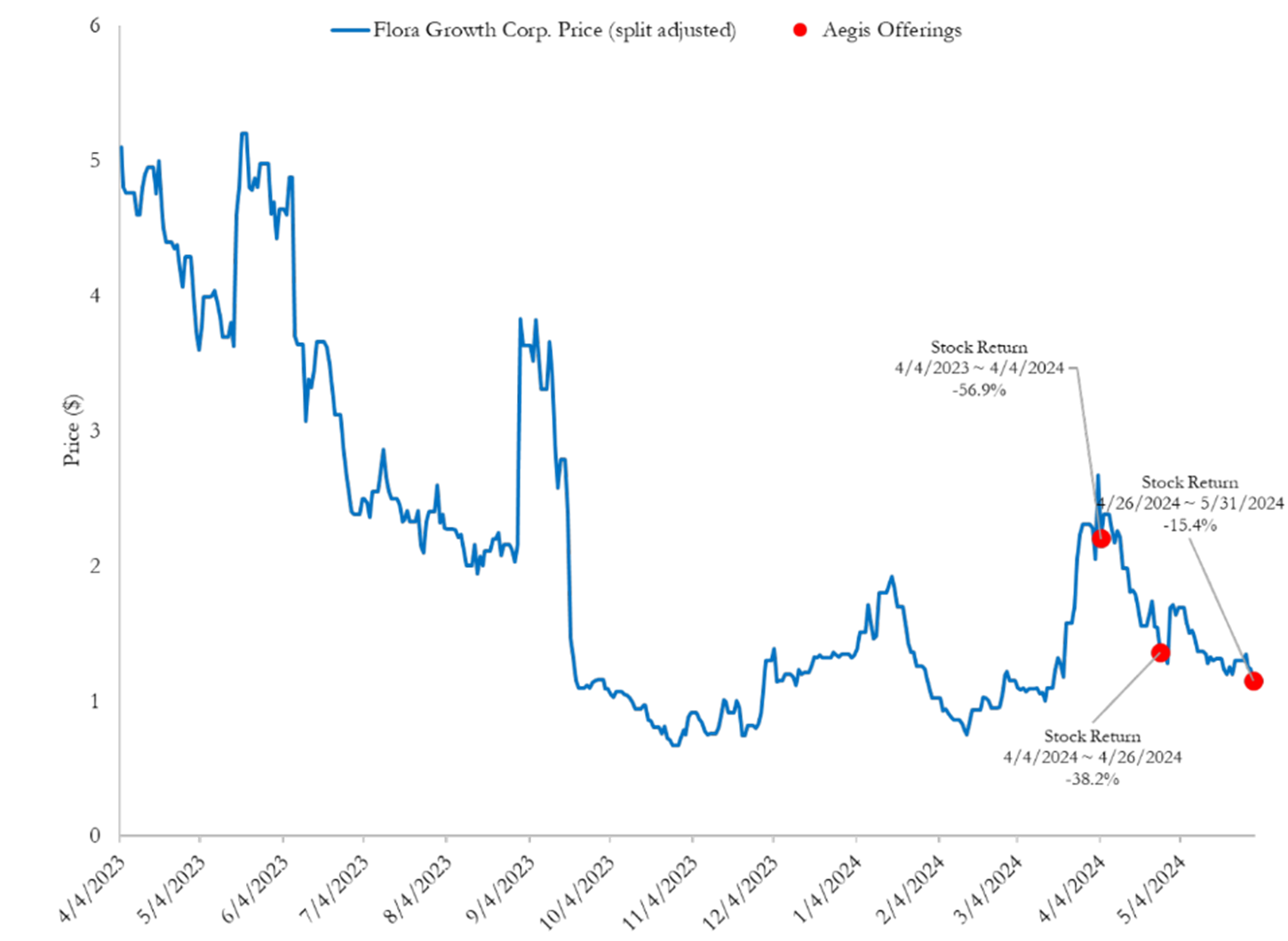

Flora Growth

Aegis underwrote two Flora Growth offerings since our March 2024 post totaling $7,014,000. The two 424bs can be located here and here.

Flora Growth's stock price had dropped 56.9% in the year prior to Aegis's first underwriting.

Flora Growth's stock price dropped another 38.2% in the three weeks between Aegis' first and second Flora Growth underwritings.

Flora Growth's stock price dropped a further 15.4% in the month between the last Sunshine Biopharma underwriting and May 31, 2024.

Cumulatively in the past two years Flora Growth's stock price has dropped 77.5% while Aegis was underwriting its securities offerings.

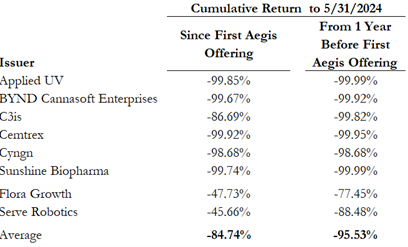

In March 2024 we published our research documenting how Aegis has caused between $3 billion and $5 billion in investor harm as a result of underwriting systematically failing nano-cap stocks. This update can be thought of as an "out of sample test" of whether Aegis truly is specialized in selling the worst securities in the market in exchange for hefty compensation and without regard to the harm it is causing to investors. This out-of-sample test confirms that Aegis continues its abusive business practices.

The eight issuers Aegis underwrote since early February have all produced disastrous results for investors.

The average cumulative returns from the first Aegis underwriting to May 31, 2024 for these 8 issuers is -87.74%. Excluding the two first time Aegis underwritten issuers, the average cumulative returns from the first Aegis underwriting to May 31, 2024 is -97.42%.

The average cumulative returns from one year prior to the first Aegis underwriting to May 31, 2024 for these 8 issuers is -95.53%. Excluding the two first time Aegis underwritten issuers, the average cumulative returns from one year prior to the first Aegis underwriting to May 31, 2024 is -99.72%.

Aegis is one of the highest risk brokerage firms in the country and is using its retail customer accounts to stuff the worst underwritings in the country. Sadly, unless some authority stops Aegis, an update later in the year will show further investor wreckage as a result of Aegis's disregard for its most basic duties.