To answer that, we examined 194 sets of offering documents for TICs sold from 2004-2009. This totaled $2.2 billion in equity, which amounts to approximately 19% of all equity issued by TICs in that period, and included properties from 32 states.

Year

Name

Issuer

State

Equity (MM)

Year

Name

Issuer

State

Equity (MM)

2004

Southtrust Tower

DBSI

Florida

$34.24

2004

Republic

DBSI

Texas

$18.10

2004

North Valley Tech Center

Argus Realty Investors

Colorado

$20.20

2004

Cypress Pointe IV

Mammoth Equities

California

$14.65

2005

Atlantic Boulevard

DBSI

Florida

$4.99

2005

Friar's Branch Crossing

DBSI

Tennessee

$7.82

2005

Lakeview & Sojourn Centers

DBSI

Texas

$16.65

2005

Renaissance Center

DBSI

Tennessee

$13.21

2005

West Michigan Industrial

Core Realty Holdings

Michigan

$23.60

2005

Westridge Executive Plaza

Core Realty Holdings

California

$8.50

2005

Bridle Creek Apartments

Geneva

Kentucky

$13.79

2005

Honey Creek Corporate Center II

Geneva

Wisconsin

$11.92

2005

Southfield Office Building

TIC Properties

Texas

$8.85

2005

Trafalgar/Avion Acquisition

Cabot

Florida

$10.70

2005

Covington Lansing Acquisition

Direct Capital Securities Inc.

Michigan

$7.38

2005

Covington Montelago Acquisition

Direct Capital Securities Inc.

Texas

$9.72

2005

Thistle Landing

Principle Equity Management

Arizona

$22.35

2005

Baylor Garland Medical Plaza

Rainier Capital Management

Texas

$5.60

2005

Professional Building - Roseville

Mammoth Equities

California

$7.72

2005

Sixth Avenue West

Triple Net Properties

Colorado

$6.60

2005

Woodside Corporate Park

Triple Net Properties

Oregon

$24.65

2005

Legacy

RMC Property

Texas

$9.78

2006

Colonnade at West Lake

DBSI

Texas

$4.95

2006

East 21st Street Buildings

DBSI

Kansas

$11.28

2006

Northpointe Tower

DBSI

Missouri

$6.74

2006

Silver Lakes

DBSI

Florida

$7.10

2006

Bridford Lake Apartments

Core Realty Holdings

North Carolina

$10.13

2006

Brookfield Lakes Corporate Center

Core Realty Holdings

Wisconsin

$32.00

2006

Cardinal Apartments

Core Realty Holdings

North Carolina

$6.34

2006

Chatham Wood Apartments

Core Realty Holdings

North Carolina

$4.39

2006

Hickory Creek Apartments

Core Realty Holdings

Virginia

$10.90

2006

Madison at Adams Farm Apartments

Core Realty Holdings

North Carolina

$11.62

2006

Park West Apartments

Core Realty Holdings

Virginia

$9.89

2006

Riverbend Apartments

Core Realty Holdings

Indiana

$30.50

2006

Sonoma Ridge Apartments

Core Realty Holdings

California

$16.00

2006

Westwind Office Park

Core Realty Holdings

California

$17.48

2006

Griffin Capital (Naperville) Investors

Griffin Capital

Illinois

$14.33

2006

Griffin Capital (Q Street) Investors

Griffin Capital

California

$21.28

2006

Griffin Capital (St. Paul) Investors

Griffin Capital

Minnesota

$19.73

2006

Griffin Capital (Naperville) Investors

Griffin Capital

Illinois

$14.33

2006

Philips Office

Moody National Companies

New Jersey

$21.04

2006

Weatherford Plaza

Moody National Companies

Texas

$9.53

2006

Chesterfield Valley Medical Office Building II

Geneva

Missouri

$8.15

2006

Honey Creek Corporate Center III

Geneva

Wisconsin

$10.45

2006

Acropolis Office Park

TIC Properties

Ohio

$11.95

2006

302 West Third Street

TIC Properties

Ohio

$8.54

2006

116 Defense Highway

Direct Invest

Maryland

$7.62

2006

Triwest Plaza

Argus Realty Investors

Texas

$17.00

2006

Residence Inn by Marriott - Chantilly

Oxford Capital Group

Virginia

$13.05

2006

Oak Grove Acquisition

Cabot 1031

Florida

$8.65

2006

DFW Office/Flex I

Equitable Companies

Texas

$10.85

2006

DFW Office/Flex II

Equitable Companies

Texas

$12.75

2006

Barrett Woods Corporate Center

Exchange Point Properties

Missouri

$9.49

2006

Springs - Office Investors

Meridian

Kentucky

$15.39

2006

Atlanta One

Moody National Companies

Georgia

$7.21

2006

Memphis Residence Inn

Moody National Companies

Tennessee

$6.93

2006

Residence Inn Lebanon

Moody National Companies

New Hampshire

$9.36

2006

Texas Two

Moody National Companies

Texas

$9.30

2006

121 Airport Centre I & II

Principle Equity Management

Texas

$16.87

2006

Business Exchange

Rainier Capital Management

Missouri

$3.19

2006

The Best Western Airport Inn Fort Myers

Gibralter Holdings

Florida

$10.69

2006

Maunakea Marketplace

Gibralter Holdings

Hawaii

$6.30

2006

Pueblo Crossing I

ORIX EMPIRE

Colorado

$6.00

2006

Fountains II And Fountains III

Wilkinson

Illinois

$7.01

2006

State Of Michigan Building

APCA

Michigan

$3.69

2006

RMC AutoSonic BMWN League City

RMC Property

Texas

$9.95

2006

State Farm Insurance Building

TIC Capital

California

$7.05

2006

Rambling Oaks Assisted Living And Rambling Oaks Courtyard

Wilkinson 1031

Oklahoma

$7.20

2006

220 Virginia Avenue

Triple Net Properties

Indiana

$20.76

2006

Las Colinas Highlands

Triple Net Properties

Texas

$15.40

2007

Beacon Point

DBSI

Ohio

$3.60

2007

Colony Commons

DBSI

Texas

$3.67

2007

Goshen Village

DBSI

Indiana

$4.74

2007

Haverford Place

DBSI

Kentucky

$7.15

2007

Park Plaza Retail Center

DBSI

Texas

$8.30

2007

Sherwood Village

DBSI

Texas

$1.94

2007

Shops @ Katy

DBSI

Texas

$4.88

2007

Village at Old Trace

DBSI

Georgia

$9.42

2007

Willow Bend

DBSI

Tennessee

$2.87

2007

Governor's Pointe

Core Realty Holdings

Ohio

$8.13

2007

Hidden Lakes Apartments

Core Realty Holdings

North Carolina

$10.50

2007

Promenade at Northridge

Core Realty Holdings

California

$11.13

2007

Revere Holdings

Core Realty Holdings

Nevada

$17.50

2007

San Antonio Airport Industrial

Core Realty Holdings

Texas

$15.10

2007

Griffin Capital (Independence) Investors

Griffin Capital

Ohio

$13.10

2007

Marriott Courtyard-Columbus Airport

Moody National Companies

Ohio

$10.81

2007

Marriott Courtyard-Columbus Downtown

Moody National Companies

Ohio

$5.85

2007

Marriott Courtyard-Lyndhurst

Moody National Companies

New Jersey

$19.22

2007

Marriott Fairfield Inn Meadowlands

Moody National Companies

New Jersey

$11.51

2007

Marriott Residence Inn-Perimeter Center

Moody National Companies

Georgia

$7.08

2007

Marriott Residence Inn-Torrance

Moody National Companies

California

$23.02

2007

Marriott SpringHill Suites

Moody National Companies

Washington

$5.83

2007

Fairfield Inn Denver (Denver One)

Moody National Companies

Colorado

$8.63

2007

Renaissance Meadowlands

Moody National Companies

New Jersey

$22.39

2007

TownePlace Suites Fort Worth

Moody National Companies

Texas

$4.58

2007

TownePlace Suites Mount Laurel

Moody National Companies

New Jersey

$5.60

2007

Beamer Place Apartments

Geneva

Texas

$10.16

2007

International Market Square

Geneva

Minnesota

$13.63

2007

Carrington Ridge Apartments

TIC Properties

Georgia

$8.55

2007

Duncan Distribution Center

TIC Properties

South Carolina

$7.25

2007

TIC N. Central Dallas Investors

TIC Properties

Texas

$5.95

2007

SBC Fenton

TIC Properties

Missouri

$6.90

2007

NNN 824 North Market Street

Triple Net Properties

Delaware

$15.00

2007

NNN Central Plaza

Triple Net Properties

Arizona

$32.80

2007

NNN Darien Business Center

Triple Net Properties

Illinois

$13.20

2007

NNN Eastern Wisconsin Medical Portfolio

Triple Net Properties

Wisconsin

$12.94

2007

NNN Exchange South

Triple Net Properties

Florida

$12.34

2007

NNN Harbour Landing

Triple Net Properties

Texas

$7.38

2007

NNN Mainstreet at Flatiron

Triple Net Properties

Colorado

$5.85

2007

NNN Old Line Professional Centre

Triple Net Properties

Maryland

$6.65

2007

NNN One Ridgmar Centre

Triple Net Properties

Texas

$11.85

2007

NNN River Ridge

Triple Net Properties

North Carolina

$10.85

2007

NNN Three Resource Square

Triple Net Properties

North Carolina

$11.48

2007

246 Omni Way

Direct Invest

Massachusetts

$12.59

2007

2810 North Parham Road

Direct Invest

Virginia

$7.82

2007

500 East Main

Direct Invest

Virginia

$16.90

2007

Braintree Park

Direct Invest

Massachusetts

$21.94

2007

Cummings Research Park - Portfolio II

Bluerock Real Estate

Alabama

$21.28

2007

Summit at Southpoint

Bluerock Real Estate

Florida

$13.55

2007

Houston Office Buildings

Argus Realty Investors

Texas

$13.62

2007

Hendersonville

Desanto Realty Group

Tennessee

$13.32

2007

Cypress Medical

Desanto Realty Group

Kansas

$10.81

2007

Clearview

Desanto Realty Group

Michigan

$9.91

2007

Fox Chase

Desanto Realty Group

Ohio

$9.77

2007

Perry's Crossing

Desanto Realty Group

Ohio

$10.07

2007

Ashtabula Acquisition

Cabot

Ohio

$15.10

2007

Northpark Southland Acquisition

Cabot

Indiana

$22.00

2007

Creekside Acquisition

Cabot

Georgia

$17.50

2007

Fontaine Business Park

U.S. Advisors

South Carolina

$11.50

2007

Courtyard Matthews & Courtyard Rock Hill

Oxford Capital Group

North Carolina

$10.33

2007

Residence Inn & Courtyard by Marriott

Oxford Capital Group

South Carolina

$11.68

2007

Residence Inn Charleston

Oxford Capital Group

South Carolina

$7.50

2007

SpringHill Suites Riverview

Oxford Capital Group

South Carolina

$5.52

2007

Crystal Lake & Pelican Pointe

Cabot 1031

Florida

$13.00

2007

East Town Acquisition

Cabot 1031

Wisconsin

$7.10

2007

Turfway Ridge Acquisition

Cabot 1031

Kentucky

$11.75

2007

Portland Senior Properties

Christopher Place

Oregon

$4.60

2007

Traverse Bay Senior Properties

Christopher Place

Michigan

$4.00

2007

Mapleridge Shopping Center

Exchange Point Properties

Minnesota

$7.72

2007

Southridge Plaza

Exchange Point Properties

Texas

$6.47

2007

Dobson Ranch

Geyser Holdings

Arizona

$4.90

2007

Yuma

Geyser Holdings

Arizona

$6.00

2007

Johns Creek Office Portfolio

Principle Equity Management

Georgia

$12.64

2007

Technology Parkway Office Portfolio

Principle Equity Management

Georgia

$13.30

2007

University Shopping Center

Principle Equity Management

Texas

$7.56

2007

Enclave Parkway

Creekstone Partners

Texas

$11.54

2007

Woodlands

Creekstone Partners

Texas

$7.36

2007

Vista Ridge

Sequoia

Texas

$9.39

2007

Forum

Sequoia

Texas

$12.00

2007

Kansas City

ORIX EMPIRE

Missouri

$8.60

2007

Battle Creek I

ORIX EMPIRE

Oklahoma

$14.00

2007

Landmark/Laumeier Office Portfolio

Bluerock Landmark

Missouri

$7.53

2007

Colonnade At King'S Grant Shopping Center

Kodiak

North Carolina

$3.85

2007

Hotel Indigo Peachtree Street

Pennbridge Capital

Georgia

$8.40

2007

Selina Plaza

TIC Capital

Florida

$2.54

2007

Northgate Business Center And Blackhawk Corporate Center

Argus Realty Investor

Arizona

$20.55

2007

Laveen Village Marketplace

Passco Companies

Arizona

$8.50

2008

Belton Town Center

DBSI

Missouri

$3.62

2008

Houston Levee Galleria

DBSI

Tennessee

$9.80

2008

Landmark Towers

DBSI

Minnesota

$16.50

2008

North Stafford

DBSI

Virginia

$13.22

2008

Peachtree Corners Pavilion

DBSI

Georgia

$3.95

2008

Pinehurst Square East

DBSI

North Dakota

$10.15

2008

Pinehurst Square West

DBSI

North Dakota

$6.36

2008

Romence Village

DBSI

Michigan

$6.51

2008

Shoppes at Trammel

DBSI

Georgia

$3.72

2008

Wisdom Pointe

DBSI

Georgia

$3.35

2008

Hunters Chase Apartments

Core Realty Holdings

North Carolina

$4.93

2008

Minneapolis Industrial Portfolio

Core Realty Holdings

Minnesota

$14.81

2008

Marriott TownePlace Suites-Portland

Moody National Companies

Maine

$9.69

2008

Cooper Glen Apartments

Geneva

Texas

$6.44

2008

NNN Jacksonville Medical Plaza

Triple Net Properties

Florida

$14.04

2008

NNN Six Forks Station

Triple Net Properties

North Carolina

$11.70

2008

NNN Washington Park

Triple Net Properties

Ohio

$12.07

2008

Heron Cove

Direct Invest

New Hampshire

$10.63

2008

1600 Barberry Lane

Grubb & Ellis

Georgia

$19.07

2008

5001 Enclave

Grubb & Ellis

Texas

$11.22

2008

Oak Park Office Center

Grubb & Ellis

Texas

$18.65

2008

2650 Old Norcross

Grubb & Ellis

Georgia

$13.66

2008

One Live Oak

Grubb & Ellis

Georgia

$17.49

2008

Plantations at Haywood

Grubb & Ellis

South Carolina

$21.36

2008

7207 Snowden Road

Grubb & Ellis

Texas

$12.36

2008

1650 Sunflower

Grubb & Ellis

California

$14.93

2008

5200 Upper Metro

Grubb & Ellis

Ohio

$6.33

2008

IBP

Argus Realty Investors

Texas

$55.00

2008

Hunter'S Chase

Desanto Realty Group

Ohio

$11.44

2008

Evanston Portfolio

Equitable Companies

Illinois

$9.49

2008

Cameron Brook Apartments

Exchange Point Properties

Georgia

$17.17

2008

Showplace

Geyser Holdings

Indiana

$5.59

2008

Madison At Fairwood Apartments

Passco Companies

Washington

$16.90

2008

Algonquin Galleria

Nelson Bros.

Illinois

$9.54

2008

Meadow Green Apartments

Delmar Equity Partners

Texas

$2.40

2008

2801 East Enterprise Drive

Whitecap Real Estate

Wisconsin

$2.38

2009

Keaau Hawaii

Geyser Holdings

Hawaii

$4.33

Showing 1 to 194 of 194 entries

After we compiled this information, a couple of things stood out. We have said before that TICs tend to have high upfront fees. In our database, the average upfront fees totaled 28% (!) of total equity. The lowest upfront fees were a still-high 17%, and the highest was a remarkable 72%. We have also said that TICs tend to be highly leveraged (i.e., use a lot of debt). Some TICs had no leverage, but both the average and median debt-to-equity ratio (total debt / total equity) across our sample was 1.56.

We've also talked about how TICs tend to have low net present values, even taking a sponsor's projected cash flows at face value. When we valued all the sponsor's projections in our database, we found that the average TIC was worth only 83.6 cents on the dollar.1 But were the sponsors' assumptions valid?

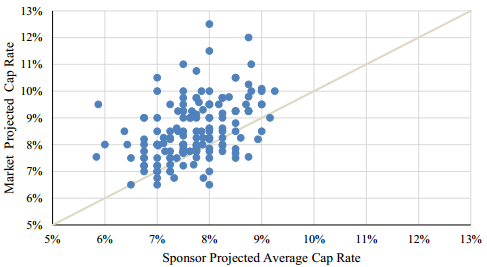

For each property, we compared the cap rate used by the sponsor to cap rates published by a real estate market analysis firm. Cap rates are used to estimate the final value of the property at sale. The lower the cap rate, the higher the resulting property value. We found that sponsors tended to use cap rates that were lower than market rates, inflating the property value at sale, as shown in the figure below (Figure 10 in the paper):

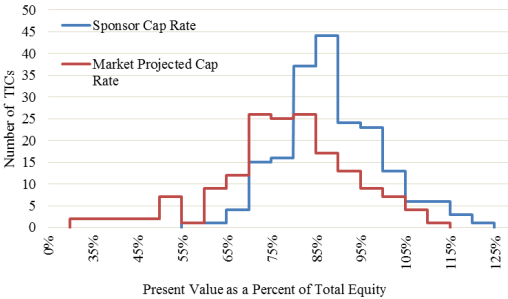

When we value all of the properties using market cap rates rather than those assumed by the sponsors, the average present value drops to 74.5 cents on the dollar. The distributions of present values before (blue) and after (red) correcting the sponsor's caps are shown below (Figure 12 in the paper):

These results suggest that TIC sponsors use aggressive assumptions when preparing cash flow projections for offering materials. These cash flows are the primary justification for projected distributions and investor returns, yet even a relatively straightforward discounted cash flow analysis reveals that most TICs were exceptionally poor investments.

_______________________________________

1 Sponsors often include multiple projections, especially for cap rate assumptions. We valued each of these alternative projections and averaged the resulting values.