Recently we've been working a lot with variable prepaid forwards (VPFs) in our casework and we decided to take a step back and explain these complex investments. A VPF is an over-the-counter contract between two parties involving a stock position, an upfront payment and option positions. VPFs are often used to defer taxes on appreciated stock, which has been a matter of somecontroversy.

Perhaps the best way to explain a complex investment is by example. Consider an investor who purchased 10,000 shares of Apple common stock (AAPL) in May 2007 for $100 and assume that at this point this position represents the majority of the investors wealth. If the investor would like to diversify her position, she would need to sell some of her stake in Apple and replace it with other securities.

If the investor sold her position now, when the shares are worth roughly $450, she would be forced to pay capital gains tax on $3.5 million ($4.5 million current value minus $1 million initial investment). As an alternative, she could enter into a VPF with a financial institution in which she would pledge the 10,000 shares to be delivered in a three years and receive an upfront payment of $3.6 million (or about 80% of their fair value).* A benefit of a VPF is that the investor can use the upfront payment to purchase other securities, potentially diversifying her overall portfolio. Also, the investor defers capital gains taxes for the term of the VPF.

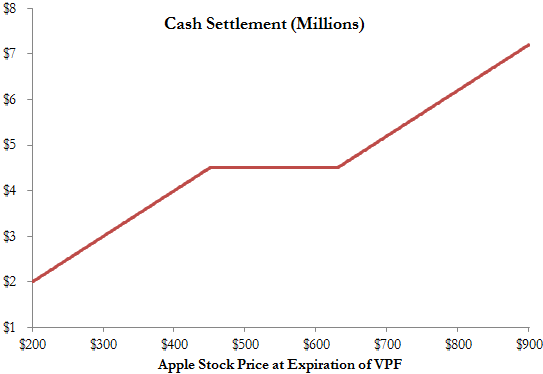

In addition to the upfront payment, the investor retains some exposure to Apple via the embedded options positions in the VPF. VPFs typically specify a "Forward Floor" (usually between 90% and 110% of the current asset price) and a "Forward Cap" (usually between 120% and 160% of the current asset price) that limit the number of shares to be delivered at the expiration of the contract. The investor remains exposed to the underlying stock for price changes between the "Forward Floor" and the "Forward Cap". Suppose that for our example the "Forward Floor" is $450 and the "Forward Cap" is $630 (140% of the current asset price).

At expiration, the investor typically has the choice of settling the contract physically (by delivering the shares) or in cash (by delivering an equivalent amount of cash). If the investor chooses to cash settle the contract independent of the final share price, then the amount she would be required to pay at the end of the contract is given by the following figure.

If the stock decreases in price beyond the floor, the investor actually benefits (she is long a put option) since less cash is required to settle the contract. If the price increases beyond the cap, the investor does not benefit (she is short a call option) since more cash would be required to settle the contract. For those with some knowledge of option strategies, this should remind you of a collar.

VPFs can be useful instruments for diversifying a concentrated stock holding or delaying the realization of capital gains taxes. On the other hand, these complex securities are often hard for unsophisticated investors to understand and often embed significant fees in an obscure way.

Frequently the compensation an investor receives (in the form of upfront payments and embedded options) may not be sufficient payment for the obligations they are taking by entering into the VPF (delivery at expiration). We covered an example of this a few months ago when JP Morgan collected over $2 million from a Trust by selling them a series of VPF contracts.

_______________________________________

*Equivalently, the upfront payment is compensation for the commitment to return the payment plus interest. The implied interest rate is determined by the upfront payment (including the value of the option positions), the current value of the pledged stock and the term of the contract.