Jun 2012

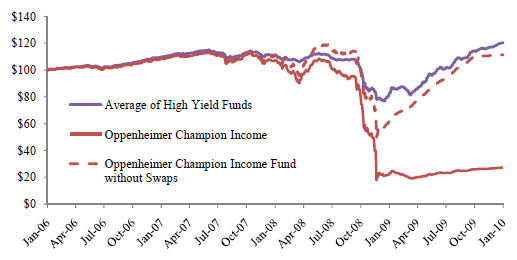

The SEC's investigation found that the Champion fund's 2008 prospectus was materially misleading in describing the fund's "main" investments in high-yield bonds without adequately disclosing the fund's practice of assuming substantial leverage on top of those investments. While the prospectus disclosed that the fund "invested" in "swaps" and other derivatives "to try to enhance income or to try to manage investment risk," it did not adequately disclose that the fund could use derivatives to such an extent that the fund's total investment exposure could far exceed the value of its portfolio securities and, therefore, that its investment returns could depend primarily upon the performance of bonds that it did not own.