Municipal bonds are debt securities issued by city, county or special-purpose government units (known as municipal authorities). This debt is typically issued to fund public works projects such as health care, construction projects or education. Because the interest from municipal bonds is usually exempt from federal income tax (one notable exception is Build America Bonds); the municipal bonds are especially attractive to high tax-bracket individuals. We will discuss some specifics of the tax-implications for municipal bonds (including state-level specifics) in a future blog post. In this post, we discuss the market yield of municipal bonds by comparing their yield to contemporaneously issued (taxable) Treasuries of the same maturity.

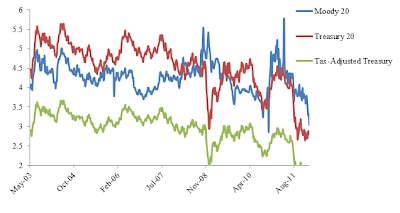

If issued at face-value, one would expect that the yield of high quality (AAA) municipal bonds should be close to the tax-adjusted Treasury yield of the same maturity: MuniYield = (1-TaxRate)*TreasuryYield. However, tax-adjusted Treasury yield is only the lower bound of the municipal yield. Empirically speaking, muni yields have traded much higher than the tax-adjusted Treasury yields. Sometimes, for example in late 2008 and 2011, the muni yields were even higher than the Treasury yields before tax-adjustments. In order to reflect the market yields, we use 20-year Moody's Municipal Bond Yield averages (Bloomberg Ticker: MMBAAAA2 Index) for municipal bonds and use 20-year U.S. Treasury Yields (Bloomberg Ticker: C08220Y Index) for comparison with taxable bonds. The maturity of each municipal bond varies, and can be as high as 40 years.

Does this phenomenon indicate an arbitrage opportunity? Our own Geng Deng and Craig McCann have shown that indeed there is no arbitrage opportunity. The difference of two yields, as explained in the same paper, can be explained by a combination of three factors: credit risk of the issuer, the embedded call option and the liquidity premium. We will discuss credit risk here, and the last two points in the forthcoming post.

Debt securities inherit credit risk from their issuers. The credit risk of municipal bonds issuers is higher than that of the U.S. government, for example. The compensation investors require for this risk is referred to as the (credit) risk premium. Before the financial crisis, the risk premium in some very high quality municipal bonds is almost zero. The financial crisis in 2007-2008 increased credit risk and amplified this premium even in the highest rated bonds. The sharp decrease of Treasury rates and sharp increase of the Moody rate around November 2008 reflects investors' sentiment concerning the credit risk of the underlying debt. We cannot ignore this risk. Perhaps the most stunning example of this risk occurred in November 2011 when Jefferson County, Alabama filed for bankruptcy. This is the largest municipal bankruptcy in U.S. history and affects over $3 billion of municipal bonds issued by Jefferson County.

Although municipal bonds are risky, they are significantly less risky than similarly rated corporate bonds. According to Moody's, the average 10-year historical cumulative default rate, from 1970 to 2009, for AAA municipal bonds is 0%, and rate for AA municipal bonds is 0.03%, comparing to 0.50% for AAA global corporates, and 0.54% for AA global corporates. In addition, the averaged recovery rate of municipal bonds, 59.91% for 30-day post-default period, is higher than those of corporates, 37.5%. The recovery rate denotes the fraction of the face-value that an investor will receive in the event of default (higher is better).

Regardless the fact that averaged risk of municipal bonds is lower than that of corporate bonds, one should still be mindful of the possibility of a municipality defaulting on their debt. If you believe the difference between municipal yield and the tax-adjusted Treasury yield can compensate you appropriately for the risks you're shouldering, then a municipal bond could be a worthwhile investment. In addition, do not forget to discuss the potential tax benefits with a tax professional.