Should You Cash Out Your Home Equity to Find Your Missed Fortune? Careful! A Scam Might Be On the Way

Feb 2012

As a result of a lifetime of thrift, many homeowners find themselves in their 50s and 60s with considerable equity in their homes. Some investment advisors and insurance salesmen have been recommending that these homeowners refinance their mortgages to take the equity out of their homes - sometime called "equity harvesting" - to purchase high cost insurance contracts or investments. Whether insurance contracts or high cost investments are being pitched, the advisors and brokers get a big pay day and homeowners end up more highly leveraged and therefore more susceptible to declines in home prices, joblessness and health risks.

For example, in October 2008 an SEC complaint charged five brokers at the World Group Securities Inc. with securities fraud, alleging that the defendants deceived customers into refinancing their homes with subprime mortgages and into purchasing variable universal life (VUL) insurance contracts. The brokers urged their customers to refinance their existing mortgage into subprime adjustable-rate negative amortization mortgages. Such mortgages usually have very low introductory interest rates, but after a period of time sometimes as short as one month, the mortgage interest rate charged increases dramatically. Paul Meyer and Craig McCann filed expert reports and gave depositions on behalf of the SEC.

VULs combine features of whole life insurance with features of mutual fund investments. A substantial portion of investors' early payments are effectively paid to the sales agent as commissions and are unrecoverable due to high surrender charges in the event the investor needs to withdraw his or her investment.

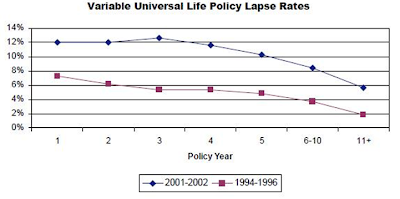

Depending on the initial premium funding, the contract's face value, the cumulating cost of insurance ("COI") and the investment returns it is highly likely the investor will abandon the investment shortly after entering into the contract. Industry experience confirms these fundamental economics. The following figure is Figure 39 from an industry study, reporting the annual lapse rates for various types of insurance policies.

Roughly half the VUL contracts are abandoned within five years and roughly two-thirds of the contracts are abandoned within ten years. Since the cash surrender value is close to zero in early years, VULs, in practice, amount to extraordinarily high cost insurance contracts which expose insurance companies to little mortality risk. VUL purchases reflect poor systematic consumer choices or systematic aggressive sales practice abuses.

"Missed Fortune 101" provides a slight twist on aggressive VUL sales. It recommends the purchase of equity-indexed universal life insurance (EIUL) policies instead of VULs with savings that would otherwise be in IRAs or in home equity. The "advice" offered by this program is profoundly bad.

Cashing out home equity to buy high cost insurance or investments dramatically increases homeowners' debts and all-in costs while systematically reducing their net worth. Only in extremely rare circumstances, especially for older homeowners, would this self-serving "advice" not be part of an abusive sales practice.